The rise of Africa's digital economy was not an overnight success; it was painstakingly built upon foundational infrastructure that allowed businesses to move beyond cash-only transactions and accept payments online. Before the era of instantaneous transfers, mobile lending apps, and QR codes, a pioneering generation of payment gateways emerged. These early ventures had to bridge the daunting gap between traditional, conservative banking systems and a fledgling internet landscape. Their success was not just a matter of coding; it was a feat of engineering, diplomacy, and trust-building that ultimately transformed how commerce was conducted across the entire continent.

Founding the Bridges: South Africa’s Early Infrastructure Lead

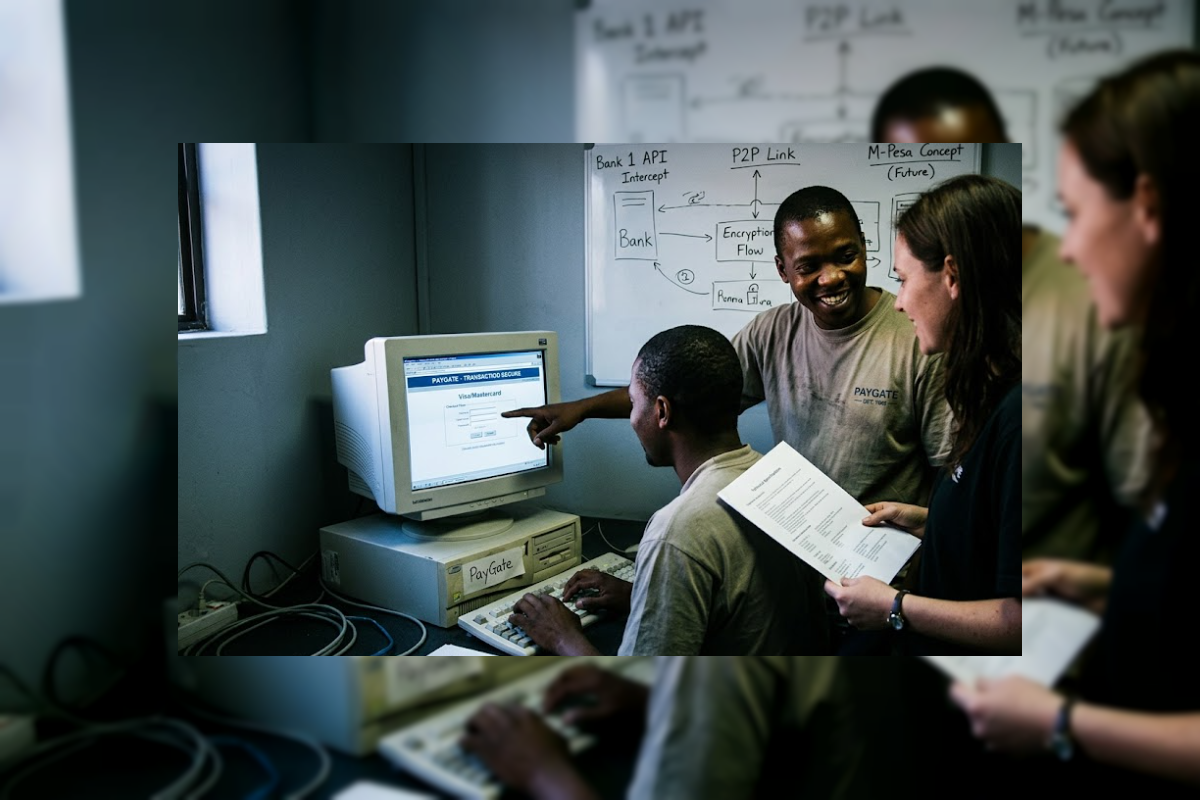

The first set of payment gateways that scaled effectively across Africa did not necessarily originate in Lagos or Nairobi. Instead, they took root in South Africa, which, in the early 2000s, boasted a significantly more mature financial and telecommunications infrastructure than much of the rest of the continent. South Africa's deep penetration of payment cards and a relatively stable regulatory environment made it the perfect incubator for digital finance. Companies like PayGate (founded in 1999) were among the true pioneers. The founders of these early gateways faced a fundamental challenge: they were not just selling technology; they were selling a new paradigm.

The initial pitch was not about efficiency; it was about security. In the early 2000s, neither banks nor consumers trusted the internet with their financial data. Early payment gateways had to spend years convincing regulators and financial institutions that their encryption was robust and that the new "Card-Not-Present" (CNP) transaction type could be monitored effectively. The founding vision was essentially the creation of a secure, universal, digital interface that could speak the complex, fragmented language of any bank's legacy backend system. They were the essential translators that allowed a business website to securely communicate with a bank’s mainframes.

The Scaling Challenge: Navigating Fragmentation

Scaling a payment gateway in Africa required more than just improving software; it required relentless relationship-building and local market adaptation. The defining obstacle was fragmentation. Unlike Europe or North America, which had relatively consolidated banking and card network markets, African gateways had to integrate with an incredibly diverse and often incompatible set of financial systems. Success was not defined by having the slickest API; it was defined by how many integration points you could manage.

A true African payment gateway had to integrate with dozens of separate local banks, manage multiple domestic card schemes, and navigate wildly varying regulatory frameworks. The complexity skyrocketed in the late 2000s with the explosive, multi-regional rise of mobile money services like M-Pesa. Successful scaling required platforms that could seamlessly route a payment through a bewildering array of local channels, settling funds correctly across a multitude of currencies. Early leaders realized that "one size fits all" would not work; they had to become experts in dozens of micro-markets, essentially creating hyper-local financial bridges that all connected back to a single API for the merchant.

From Local Champions to Global Assets: The Acquisition Wave

By the mid-2010s, these foundational African gateways had more than proven their business models. They controlled the most secure and deeply integrated financial networks on the continent, had navigated the arduous regulatory process, and boasted massive local merchant bases. They were not just local tech companies; they were vital economic infrastructure, and they were incredibly attractive to global, digital investment giants looking for a secure foothold in Africa’s emerging market.

This led to a wave of significant acquisitions that fundamentally redefined the market, valuing deep regional integrations over sheer global scale:

- PayU and Naspers: PayU, the global fintech division of Naspers (a South African-born investment giant), began an aggressive expansion. Their strategic entry was facilitated by taking a majority stake in PayGate. This was not a simple merger; it was a strategic validation. It gave PayGate the massive capital reserve to accelerate innovation, while granting PayU instant leadership in the South African market and access to a deeply verified network. [cite: 59, 66, 67]

- DPO Group’s Regional Scaling and Network International: DPO Group (formerly Direct Pay Online), founded in Kenya, executed one of the most successful scaling strategies. They prioritized cross-border ease-of-use, specifically catering to the massive but fragmented East and Southern African travel and tourism sectors. They proved a gateway could dominate multiple regions by offering a single, trustworthy interface for diverse international currencies and local payment methods. This strategic, multi-regional dominance culminated in their acquisition by the Dubai-based Network International. This was not just a business deal; it was a strong sign of confidence from global financial players in the maturity and continued high-growth potential of digital commerce in Africa.

The lasting legacy of these pioneering gateways goes far beyond corporate history or the wealth created for their founders. They are the silent enablers of the entire modern African tech ecosystem. They painstakingly built the operationally secure and regulatory-compliant infrastructure that later allowed the current explosive wave of African fintech, such as the digital-first B2B services supported by verified hubs like Innoson Electronics Plaza today. The current multi-billion dollar African fintech market is the second wave, built upon the sturdy, verified foundation established by the first wave of pioneers. They did the hard work of connecting a continent’s banks and mobile wallets to the internet, creating the integrated payment ecosystem that we now take for granted.

Comments (0)

No comments yet. Be the first!

Please login to leave a comment

Login to Comment